New Car Market Shift

It might be surprising, given the flood of young faces in auto ads, but fewer young people are driving away in new cars these days. The share of new car buyers aged 18-34 has sunk to less than 10 percent, from around 12 percent just a few years back. In the meantime, older folks, those 55 and up, have taken command over nearly half of new car sales, up from 45 percent.

Cost Challenges

A key factor is cost. The monthly payment for a new set of wheels has jumped by 30 percent over the last four years, pushing the average over $1,000 per month for one in five cars. That’s a daunting figure when coupled with the re-emergence of student loans, a challenge specific to the younger crowd.

Used Cars in Demand

These pricing pressures drive younger buyers to seek solace in the used car market, where monthly payments and insurance are more manageable. With urban environments offering more ride-sharing and public transport options, some are opting out of car ownership entirely.

Future of Car Ownership

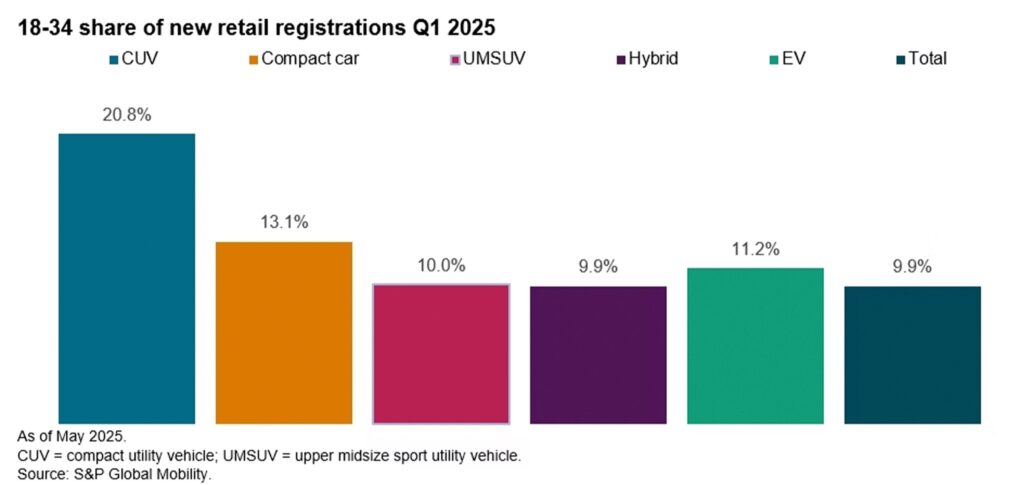

It’s a scene ripe for change. Some car manufacturers envision a decrease in ownership, predicting that younger generations are simply ahead of the curve. Currently, the desire for compact utility vehicles tops the list for those still buying new, with compact cars trailing right behind. However, future budget-friendly electric vehicles from automakers like Ford and VW might shake things up, potentially revamping the current buying trends among the young.

In wrapping up, despite the downturn in new car statistics, younger buyers still contributed to 1.1 million new vehicle registrations recently. It’s a dynamic market, and as EV technologies become more financially accessible, who knows? There might be an uptick among these young drivers sooner than expected.

Tesla Leads EV Market

Lucid Teases New EVs

Mercedes Recalls

Electric M3 Unveiled

CEO Pay: Stellantis Edge